The first-year 183-day NLV rule explained

Hold the press! As of around 16 June 2026 it’s been deemed that the 183-day ‘rule’ for denying residency renewals cannot be used. The reasoning is that the requirement was merely a bylaw, not a law, and therefore is unenforceable, according to the high court.

It means that if you’re out of Spain for more than the 183 days in your first 12 months (or any other year) you should still be eligible for renewal. Questions remain as to how long it will be for regional immigration offices to notice this. It might be that, wrongly, a few people might still be denied. But the law is on your side, so if you’re one of the people who’s been denied on the 183-day rule you should appeal, or re-appeal.

All the other requirements still apply, namely the need to have continuous health insurance and sufficient financial means.

There’s still discussion going on around the requirement for tax residency, i.e. can you qualify for residency renewal even if you’re not a tax resident in Spain?

The bad news is that all the time I spend working out the 183-day requirements has been wasted. Anyway, don’t bother reading further. For now.

They say that you only truly understand something if you can explain it to your cat. Or something.

Anyway, here’s how I explained to Ted the mysterious rule that underpins the requirements for the Spanish non-lucrative visa, the one that says thou shalt reside in Spain for at least 183 days in order to successfully reapply for residency the following year.

This post won’t appeal to very many people, but then I’ve never been one to pander to popularity. Just ask everyone I went to school with.

I wrote it because one of the rules of maintaining your residency in Spain after acquiring an NLV is that you must be in Spain for 183 days or more of each calendar year. (For the purposes of this post I’m ignoring the requirement for long-term residency, for which you are entitled to apply only if you have spent no more than 10 months outside of Spain in the five-year period from your first arrival.)

It is now a requirement for continued NLV residency that you become a tax resident of Spain, which is triggered when you spend 183 days* or more within a calendar year, the calendar year also being the Spanish financial year.

At face value, both these requirements seem to line up with no problem. It makes sense. Until you think about the date on which you first arrive.

If, for example, you arrive in Spain in the latter half of the year – 2 July to 31 December (which spans 182 days) – by definition you will not become a tax resident in that year. There are fewer than 183 days left. That’s no one’s fault, and you can slide on through to the following year and begin dealing with tax then. This is really important to know if selling a property in your home country could incur capital gains tax in Spain – sell your house, then move to Spain after 2 July, then you won’t be liable for capital gains tax in Spain.

But I was confused about something. I made up an imaginary scenario and posted it to an NLV Facebook group to see whether I could coax someone knowledgeable to chip in. You see, to date, when people have innocently asked about this rule and how it applies in their case, they are usually bombarded with unhelpful responses like ‘You have to spend 183 days in Spain’. ‘In a calendar year.’ ‘In your first year.’

The (often unintentional) ambiguity is palpable, frustrating, and really grinds my gears. Luckily, this time around came a few well-considered comments that have helped me understand how it all works.

Here’s my imaginary scenario, with the full case written below.

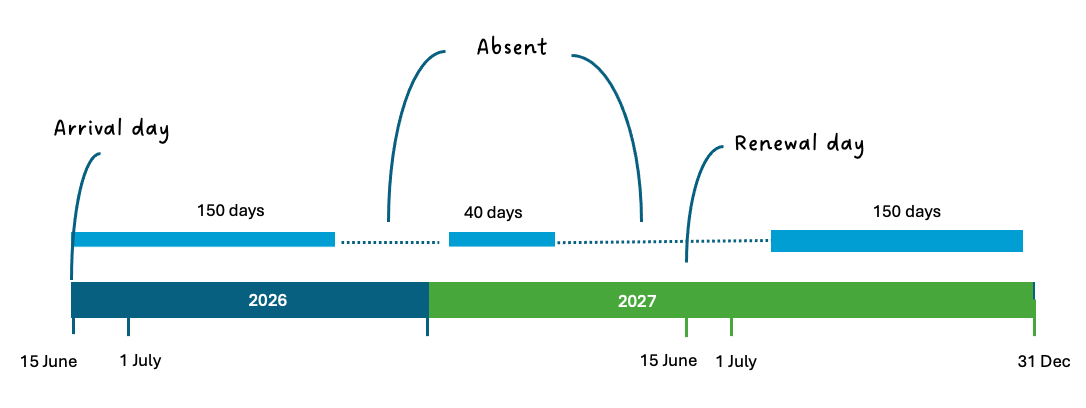

NLV recipient Barry arrives in Spain on 15 June 2026, then spends 150 days of 2026 in Spain before going ‘home’ to Timbuktu to visit family for the rest of 2026. He then arrives back in Spain in early 2027 and stays for 40 days, leaves and does not return until the latter half of 2027.

In the period from 15 June 2026 to 15 June 2027, Barry has spent 190 days in Spain and therefore qualifies for his NLV renewal on 15 June 2027 (for which he applies well within the allowed 90 days post expiry, on the day he enters Spain again).

But, by the time of that renewal he has not yet spent 183 days or more in the single calendar year of 2026 or 2027 – even though he could have, had he not left the country that first time. In other words, at the time of NLV renewal Barry believes that he has not yet become a tax resident but has still met the requirements for renewal.

The end.

The question of how tax residency applies to Barry occurs to lots of folks, judging by the number who post on the various NLV groups; predominantly they’re worried about the aforementioned capital gains tax situation. My scenario quickly had its flaw pointed out by a poster called David, who really seems to know his onions.

David says that while indeed Barry did not spend 183 days of 2026 in Spain, for the purposes of tax residency the government considers his absence temporary, and that he will be considered a tax resident for 2026. Poster Howard points to the newly rewritten law (May 2025), which says that in order to qualify for visa renewal you must be considered …

‘[t]o have resided in a real and effective manner in Spain for more than one hundred and eighty-three days during the calendar year.’ [Translated from Spanish, my bold]

‘Real and effective manner’ being the key term, and the consensus seems to be that it means simply: You live here now and bugging out for a few weeks ain’t going to cut the mustard.

So it looks like Barry is screwed, and would likely be denied renewal were he to fail to lodge a tax return in Spain for 2026.

Who says law is boring.**

* The legislation on NLV and tax is separate. Somewhere I read that for the latter the count is 184 days, but this doesn’t affect the point of this post.

** This is a rhetorical question.